Have you ever asked yourself, “How much money do I need to retire comfortably?” If so, you’re definitely not alone, and it’s something that I have calculated many times as well! This is one of the most common money questions I hear, and I completely understand why. Planning for retirement can feel overwhelming, especially when…

Have you ever asked yourself, “How much money do I need to retire comfortably?” If so, you’re definitely not alone, and it’s something that I have calculated many times as well!

This is one of the most common money questions I hear, and I completely understand why. Planning for retirement can feel overwhelming, especially when you see people throwing around numbers like $1 million, $2 million, or more. But the truth is, there’s no one-size-fits-all answer.

What matters most is your personal lifestyle, spending habits, and retirement goals.

Best Ways To Calculate How Much Money You Need To Retire Comfortably

In this article, I’m going to break this topic down into easy steps so you can start figuring out your own retirement number without feeling stressed, confused, or like the whole thing (retirement) is impossible.

Recommended reading: How To Save For Retirement – Answers To 13 Of The Most Common Questions

1. Think about what “retire comfortably” means to you

Retirement, and even retiring comfortably, will mean something different to everyone.

Before you figure out how much money you need, you first have to think about what a comfortable retirement looks like for you.

For some people, that means traveling the world, going on cruises (such as expensive world cruises!), or spending winters somewhere warm. For others, it might mean downsizing to a smaller home, enjoying hobbies like gardening or reading, and spending time with grandkids.

Retirement looks different for everyone, as you can see.

Here’s a good exercise to do – think about one full day in your dream retirement and questions like: What time do you wake up? What do you eat? Are you relaxing, traveling, or working a part-time job you like? Are you living in the same house, or have you moved to a smaller space or a new city?

Then, write down what kinds of expenses go along with the lifestyle you’d like to live. This can help you determine whether you’ll need more or less than the “standard” retirement number recommendations.

You can also make a list of things you want in your retirement, such as a travel budget, helping your kids or grandkids, or keeping a second home. Then, build your retirement plan around those core goals.

2. Retirement rules of thumb (kept simple)

There are a few helpful rules you can use to estimate how much money you might need to retire. These aren’t perfect and I did simplify this a lot, but they’re a good place to start.

- The 25x rule – Multiply your expected yearly costs by 25. So, if you want to spend $40,000 a year in retirement, then you’ll need $1,000,000 saved.

- The 4% rule – This means you can withdraw 4% of your retirement portfolio each year without running out of money too quickly. So, if you have $1 million saved, you could withdraw $40,000 per year.

Okay, I know these two rules sound similar, and that’s because they are! The 25x rule focuses on how much to save before your retirement. The 4% rule, on the other hand, focuses on how much you can safely withdraw from your retirement savings each year in retirement.

Now, I do want to say that these rules usually work best if your money is invested and continues to grow during retirement (hello, compound interest!). If you’re planning to live off cash savings alone, or if you want to keep everything in low-interest accounts, you will most likely need to save more because your money won’t be growing.

Recommended reading: What Are Dividends & How Do They Work? A Beginner’s Guide

3. Estimate your retirement expenses

Knowing how much you think you’ll need is one thing, but actually understanding your expenses is where the real planning begins.

Start by tracking your current monthly expenses.

Break them into categories like:

- Housing: rent/mortgage, property taxes, home maintenance/repairs, and HOA fees

- Utilities: electricity, gas, water, internet, phone, and sewer

- Food: groceries and restaurants

- Transportation: gas, car insurance, car payments, and repairs

- Health: insurance premiums, prescriptions, copays, dental, and vision

- Travel and fun: vacations, hobbies, and entertainment (like listening to live music or going to the movies)

- Personal: clothing, haircuts, gifts, and subscriptions

Once you’ve got your current budget, ask yourself: Will this increase, decrease, or stay the same in retirement? I know it’s hard to estimate now, but the first year of retirement may look completely different in terms of expenses than you think if you don’t plan for it.

Some expenses will likely go down, like commuting, childcare, or business attire. But others, such as healthcare and travel, might go up. The amount that you spend on hobbies may go up as well because you will have more free time. Don’t forget about inflation, either. A dollar today won’t buy as much 20 or 30 years from now.

So many people assume that they will spend less in retirement, but that’s not always the case. Many people spend more money!

4. Will you work or earn income in retirement?

Not everyone wants to stop working completely.

In fact, many retirees choose to work part-time, freelance, or start side hustles in retirement. I think doing something you like, even if it’s just a few hours a week, can make you extra income and also make you happy.

Here are some retirement side hustle ideas:

- Teach music lessons, tutor, or babysit

- Sell crafts or handmade items on Etsy

- Do freelance writing, bookkeeping, proofreading, or virtual assistant work

- Work at a national park, museum, or store

- Consult for businesses

Even bringing in $500 to $1,000 a month can help stretch your savings and give you more financial freedom. It can also allow you to retire earlier or spend more freely.

I think a great task for this section is to ask yourself: Would you want to do a small amount of work in retirement if it helped you retire sooner or travel more?

Recommended reading: 17 Best Retirement Side Hustles

5. Where you live matters

Your location can have a huge impact on how much money you need to retire comfortably. This is because living in a high-cost-of-living area means you’ll need more money saved so that you can afford your expenses.

Some retirees choose to:

- Move to a smaller home

- Move to a lower-cost state with no income tax (like Florida or Texas)

- Relocate to a walkable community and go car-free (many towns give out free or heavily discounted public transportation passes too!)

- Move abroad to a country with a lower cost of living

For example, someone living in San Francisco will likely need much more in retirement savings than someone living in rural Tennessee. Housing, healthcare, groceries, and more can all vary so much, even within the same country.

6. Don’t forget about healthcare

Healthcare costs tend to rise as you age (plus, they are rising for just about everyone anyway!), and they can eat up a big chunk of your retirement budget if you’re not prepared.

While Medicare can help pay for many expenses after the age of 65, it doesn’t pay for everything. You may still have to pay for:

- Copays and deductibles

- Dental and vision care

- Prescription drugs

- Long-term care or in-home help

One way to plan ahead is by using a Health Savings Account (HSA) if you’re eligible. HSAs have great tax benefits: your contributions are tax-deductible; they grow tax-free; and withdrawals for medical expenses are tax-free too.

I personally have a friend who retired but then went back to work part-time (for the same employer) so that their family could have free health insurance (their employer paid for health insurance). So, this may be something to look into as well.

Recommended reading: 15 Part Time Jobs With Health Insurance

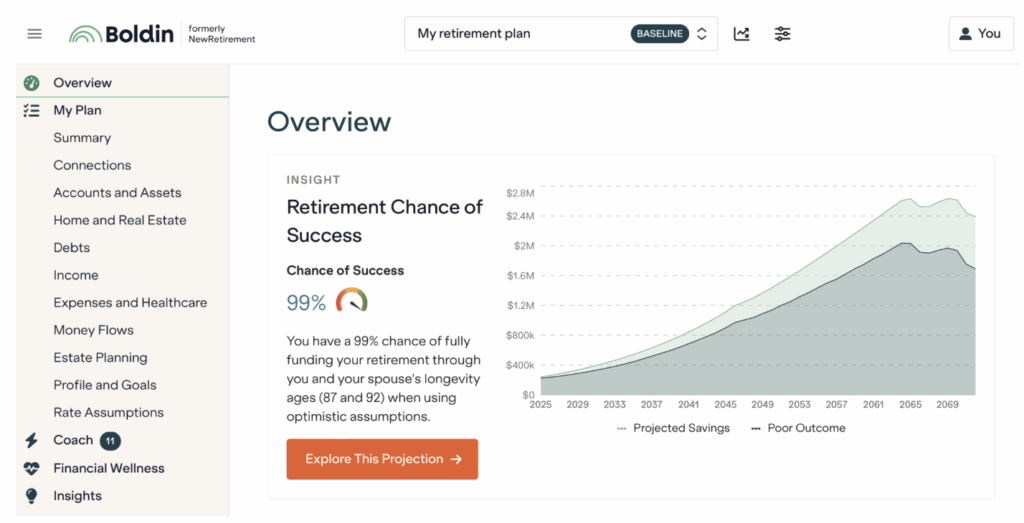

7. Tools to help you figure out your retirement number

If you’re not a spreadsheet person or don’t want to use a financial advisor, don’t worry, there are lots of free tools that can help you figure out your retirement number on your own.

One popular tool is Boldin. I recently tested it, and I loved how simple it was. You can link your accounts or enter your income and savings manually. It gives you an easy-to-understand picture of your progress toward retirement and even suggests how to improve your retirement plan.

You can click here to start a free Boldin account and use their retirement calculator and platform to:

- Learn what age you can retire

- See your net worth

- Calculate your estimated retirement income and expenses

- Figure out the best age to get Social Security

And more.

Another popular free option to plan your retirement is with Empower (this used to be called Personal Capital).

It’s okay if you’re not there yet

If you’re reading this and thinking, “I’m so far behind, I’ll never retire,” please know that you are not alone, and it’s never too late to start.

The important thing is to start today, even if it’s just a small step like reading this article!

Here are a few other ways to get started:

- Increase your retirement contributions

- Open or max out a Roth or 401(k)

- Eliminate debt to lower your monthly expenses

- Downsize your home or car

- Look for ways to earn extra income and invest it

- Find part-time work in retirement to make your retirement savings last longer

Now, I do want to say that you do not have to be perfect and every little bit helps. The earlier you start, the more time your money has to grow, but even starting later can still lead to a comfortable retirement.

So, just start!

Frequently Asked Questions

Below are answers to common questions about how to figure out how much money you need to retire comfortably.

Can you retire at 60 with $500K?

This depends on your lifestyle and whether you have other income sources like Social Security or a pension. If you live in a low-cost area and keep your spending low, then it’s possible, but I think it’s always helpful to have a plan!

Can you retire with $1.5 million comfortably?

Yes, for many people this is more than enough in a retirement account, especially if you spend around $60,000 or less per year. This amount gives you flexibility, especially if your home is paid off and you don’t have other debt.

Is $300,000 enough to retire on with Social Security?

It could be enough for a modest retirement, especially if you live in a low-cost area and you have Social Security benefits. However, it may require some budgeting.

Can I retire at 55 with $2 million?

Possibly, yes! It really depends on how much money you spend each year to know if the $2,000,000 will last you. But, for many people, this is more than enough money to save for retirement.

Is $40,000 a year enough to live on in retirement?

Whether or not $40,000 a year is enough to live on in retirement depends on your location, lifestyle, and whether your home is paid off. Many retirees live on this amount or less, but it just depends on you and your spending.

What is a good monthly income in retirement?

A good monthly income depends on many things, such as your retirement lifestyle (do you want to travel? have any expensive hobbies?), where you live (California and Hawaii are typically going to be more expensive than Arkansas, for example), and whether you have debt.

Can I retire without a mortgage?

Yes, and many people plan their retirement around paying off their homes. I think it’s a great goal to have because, without a mortgage, your monthly expenses can be much lower, making it easier to live on a fixed income that is lower.

Do I need to factor in inflation when planning for retirement?

Yes! Prices for everything, like food, housing, and healthcare, go up over time. If you need $50,000 per year today, you may need $65,000 or more in 10 to 15 years. So, make sure your retirement plan grows with inflation.

How Much Money Do You Need To Retire Comfortably? – Summary

I hope you enjoyed my article on how to figure out how much money you need to retire comfortably.

Personally, this is something I think about all the time. I’ve spent years creating a life and business that gives me freedom and flexibility. But retirement crosses my mind (all the time, to be honest – I feel like this is normal for a financial expert, ha), especially now that I have a daughter and want to make sure we’re financially free long-term and forever.

There’s no exact retirement number that works for everyone, so understanding your own lifestyle, expenses, and goals will help you create a plan that works for you.

For some people, the number may be $500,000, and for others, it may be $5,000,000. I personally know people who have retired on each of these amounts and some who have retired on even less as well. And, they are all happy!

What does your dream retirement look like? Have you figured out your retirement number yet?

Recommended reading: